5 Compliant Debt Validation Letter Templates and Samples

Beyond defining inconvenient collection times, types of letters to send and where to send them…there’s one specific requirement from the Act that’s a pain point for organizations trying to collect from debtors. Debt validation letters. Here are 5 FDCA-compliant debt validation letter templates and samples.

50% of Americans failed to consistently pay all of their bills on time in 2022 according to Consumer Affairs.

Meanwhile, Intuit found that 64% of small businesses have recieved a late fee specifically due to cash flow issues.

In other words, it doesn’t matter what side of the coin you’re on, whether you’re a business owner or an average consumer, the odds that you’re affected by debt aren’t in your favor.

Since both consumers and businesses consistently fail to pay their bills, it makes sense that the debt collection industry continues to grow. More specifically, the debt collection industry has seen an average growth rate of 2.6% percent since 2017.

And as more organizations and consumers fail to pay their bills consistently, that industry growth rate is only going to continue to climb.

Although it gets a bad rap and oftentimes receives comparisons that it’s akin to noir gangster movies, the collections industry is highly regulated.

Like the industries that collections agencies serve, they also have to stay compliant with government mandates to operate. If they don’t they risk massive fines that could close their doors forever.

Of course, the specific regulation I’m referring to is the Fair Debt Collection Practices Act (FDCA). If you already work within the collections space, you’re very familiar with what the Act requires. In short, the Act spells out what is and isn’t allowed by organizations that collect debts.

Beyond defining inconvenient collection times, types of letters to send and where to send them…there’s one specific requirement from the Act that’s a pain point for organizations trying to collect from debtors. Debt validation letters.

Just because they’re a requirement, though, doesn’t mean you can’t use them as a means to collect sooner. Here are 5 FDCA-compliant debt validation letter templates and samples.

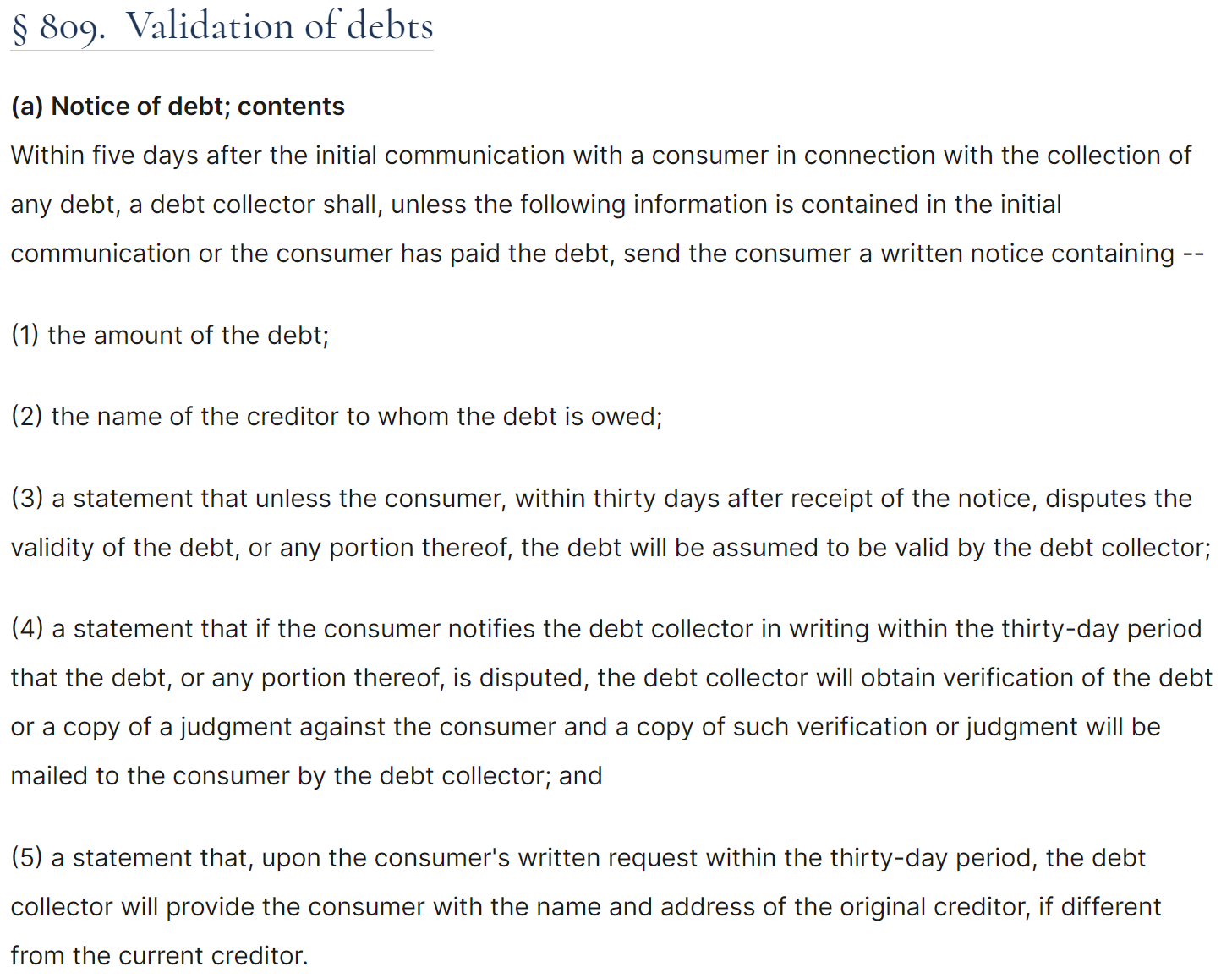

Debt Validation Letter Requirements

You see, section 809 of FDCA requires that collection agencies send a “validation of debts” within 5 days after the initial contact with the consumer.

But, what type of information should exist in a debt validation letter? Luckily, the law also spells that out.

To be compliant with the FDCA, debt validation letters MUST include the following information…

- The amount of debt owed

- The name of the creditor that requests the debt

- A statement that states the assumption of the validity of the debt unless it’s disputed within 30 days after receipt

- A statement that details that if the consumer sends a dispute letter in writing to the collector about the debt within 30 days, the collector will verify it and mail the verification to the consumer

- A statement that details that upon the consumer’s written request the debt collector will provide the name and address of the original creditor

Pretty straightforward, right?

Well, the reality is that there’s one caveat in the FDCA that most collections agencies follow when creating their debt validation letters.

Within the first part of section 809, the FDCA states that a debt collector doesn’t have to create and send a debt validation letter if the initial communication with the consumer contains the required information.

As such, many collections agencies opt to stay in compliance with FDCA’s debt validation requirements with the first correspondence to the consumer.

But, what should those look like?

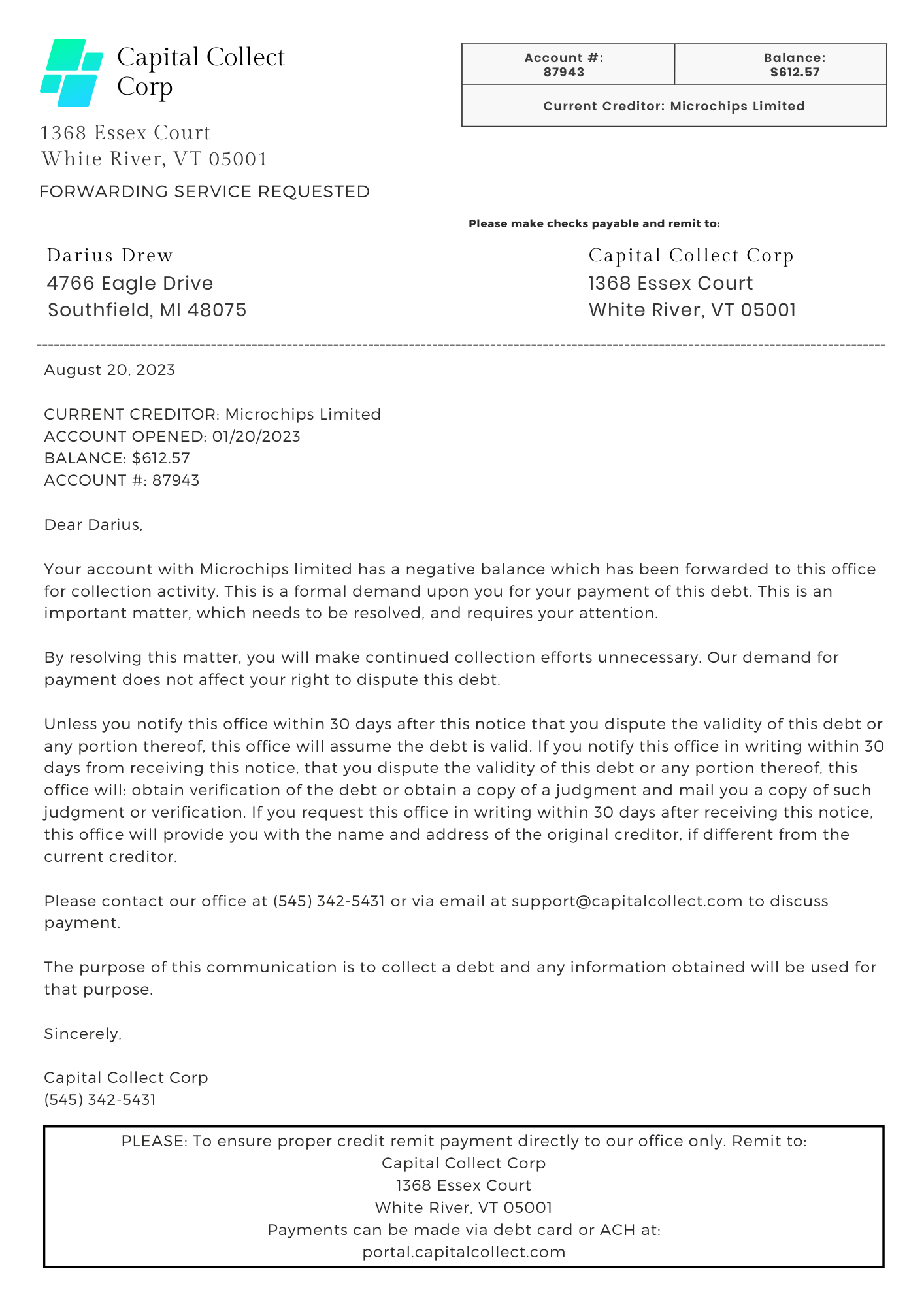

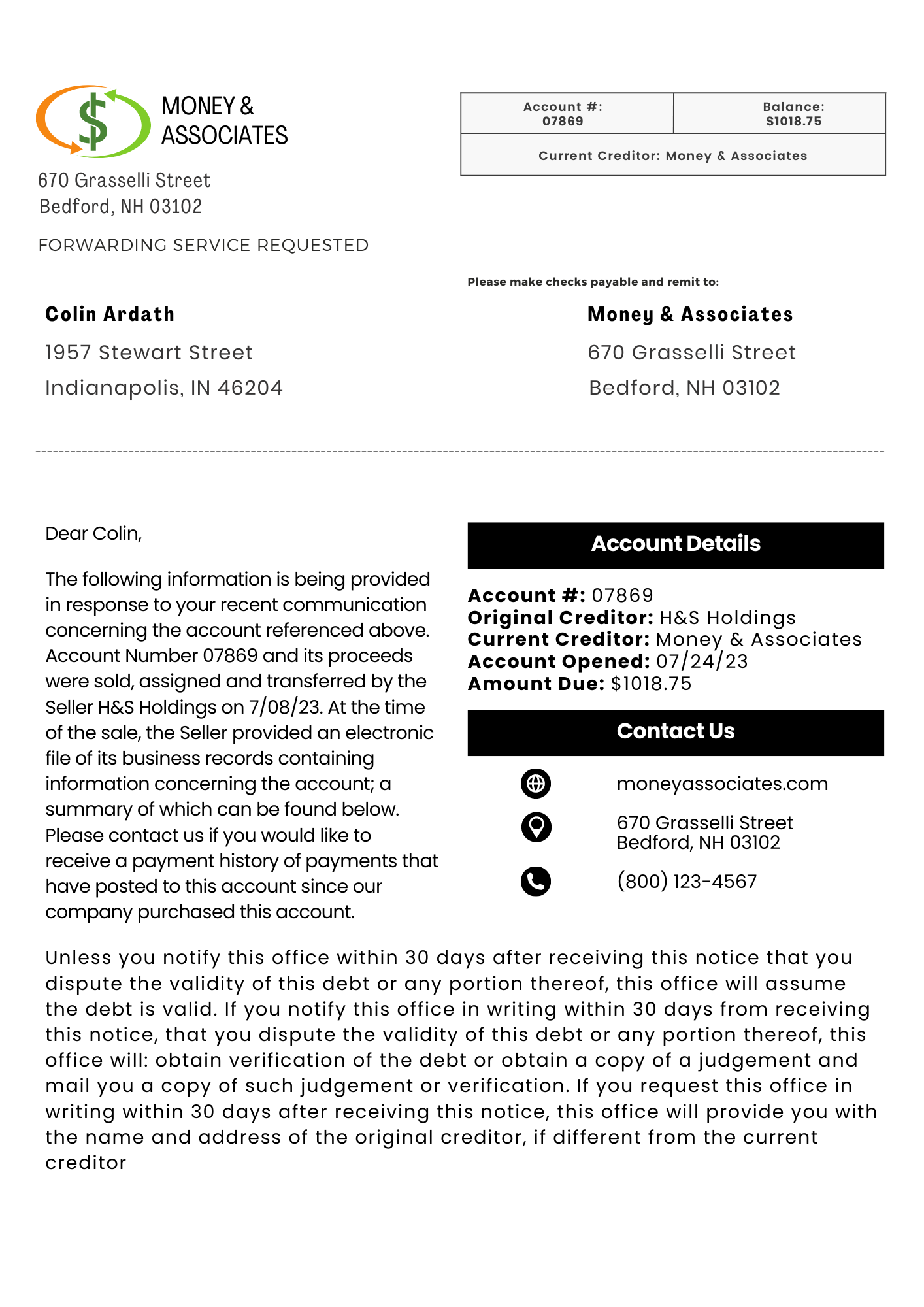

Debt Validation Letter Template 1: Initial and Compliant

The first sample I have for you focuses heavily on ensuring compliance with FDCA’s debt validation letter requirements.

It takes on the form of a professionally-styled letter with two objectives. First, notify the recipient of their outstanding balance with a specific creditor. Second, explain the rights associated with what’s required by the law.

It’s a pretty standard looking sample and it's effective. Yet, I maintain that there are better templates to take advantage of.

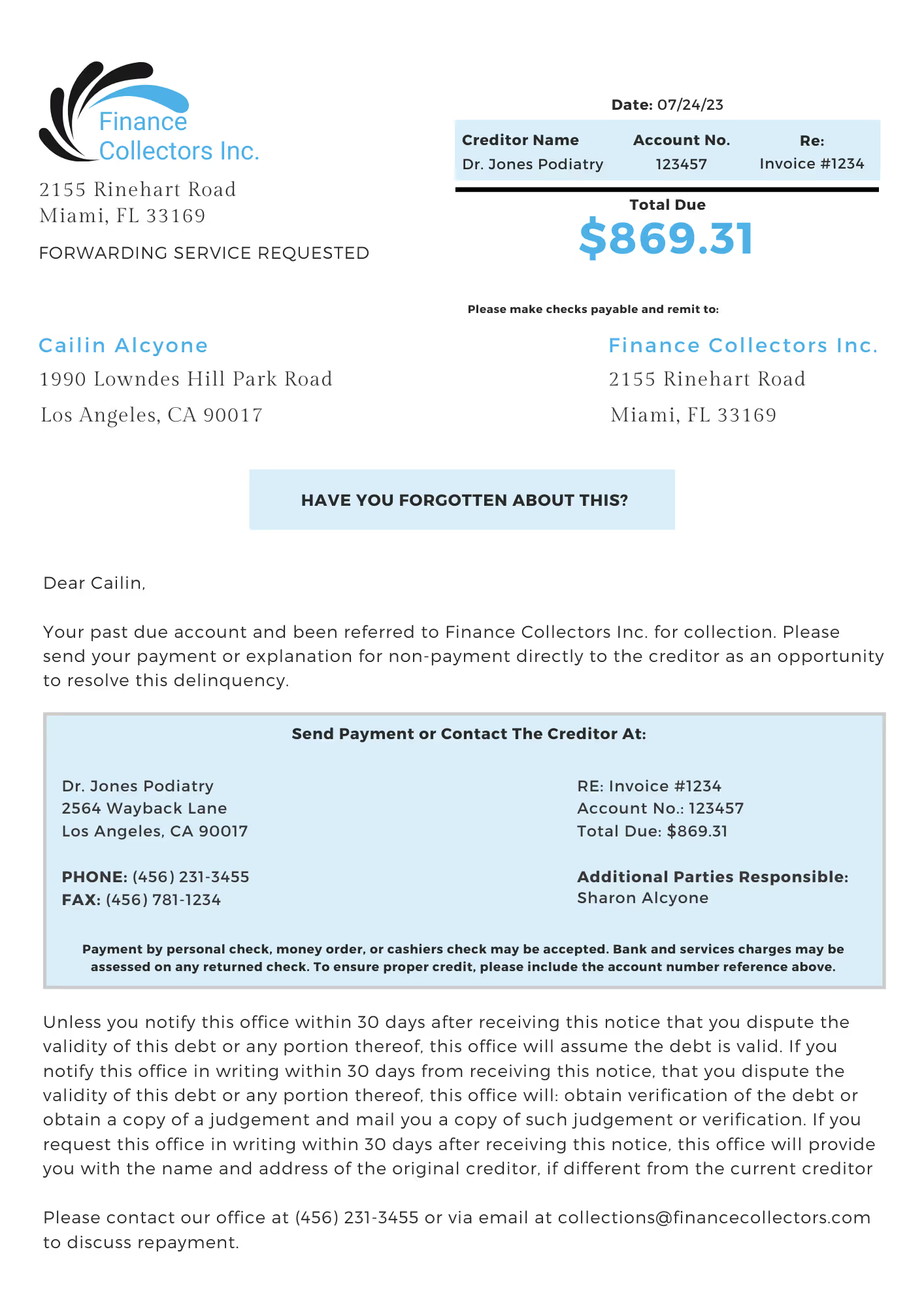

Debt Validation Letter Template 2: Designed for Readability

Yes, as a debt collector, you have to ensure that what you send to consumers is compliant with FDCA’s guidelines. But that doesn’t mean what you send can’t include visual elements to draw the reader towards specific parts of the debt validation letters you send.

This second template does exactly that, draws the recipient in.

What are the two most important aspects that you need to communicate to individuals who have outstanding balances? The answer to that question is simple: what’s owed and how to pay.

The truth is that if you’re sending physical letters to consumers, you have a lot of noise to compete with.

In 2021 alone, the USPS sent almost 51 billion pieces of First-Class Mail.

Since your organization’s job is to collect on behalf of others, you need to do whatever it takes to make the letters you send stand out.

To stand out in such a crowded direct mail landscape, you need to consider design elements.

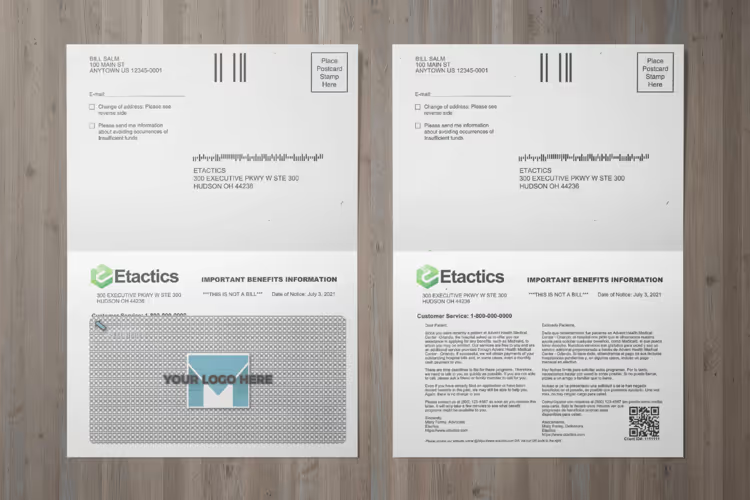

Debt Validation Letter Template 3: Remits for Returns

For your recipients to satisfy the balance that they owe, you need to provide them with a way to send their payment back to you through the mail.

Beyond enclosed a prepaid envelope inside with the letter that you send, that also means you need to use remits.

In the statement and invoice world, a remit is usually a portion at the top or bottom that requests the recipient to tear off and send back alongside their payment

I need to come clean to you. The majority of samples I’ve provided for you thus far have remits on them.

Did you notice the dotted line towards the top of the first sample? That dotted line represented a perforated edge that the recipient could tear off, include inside the prepaid envelope and mail back to you. That’s a remit.

The ultimate purpose of a remit is to allow the recipient to write in credit card information and send it back to you. Sample 1’s remit provided that table on the back.

However, it might make more sense to provide the credit card box on the front of the validation letters you send out. That way it’s more obvious that you accept credit card payment and that all they have to do is fill it out, tear the edge and mail the remit back to you.

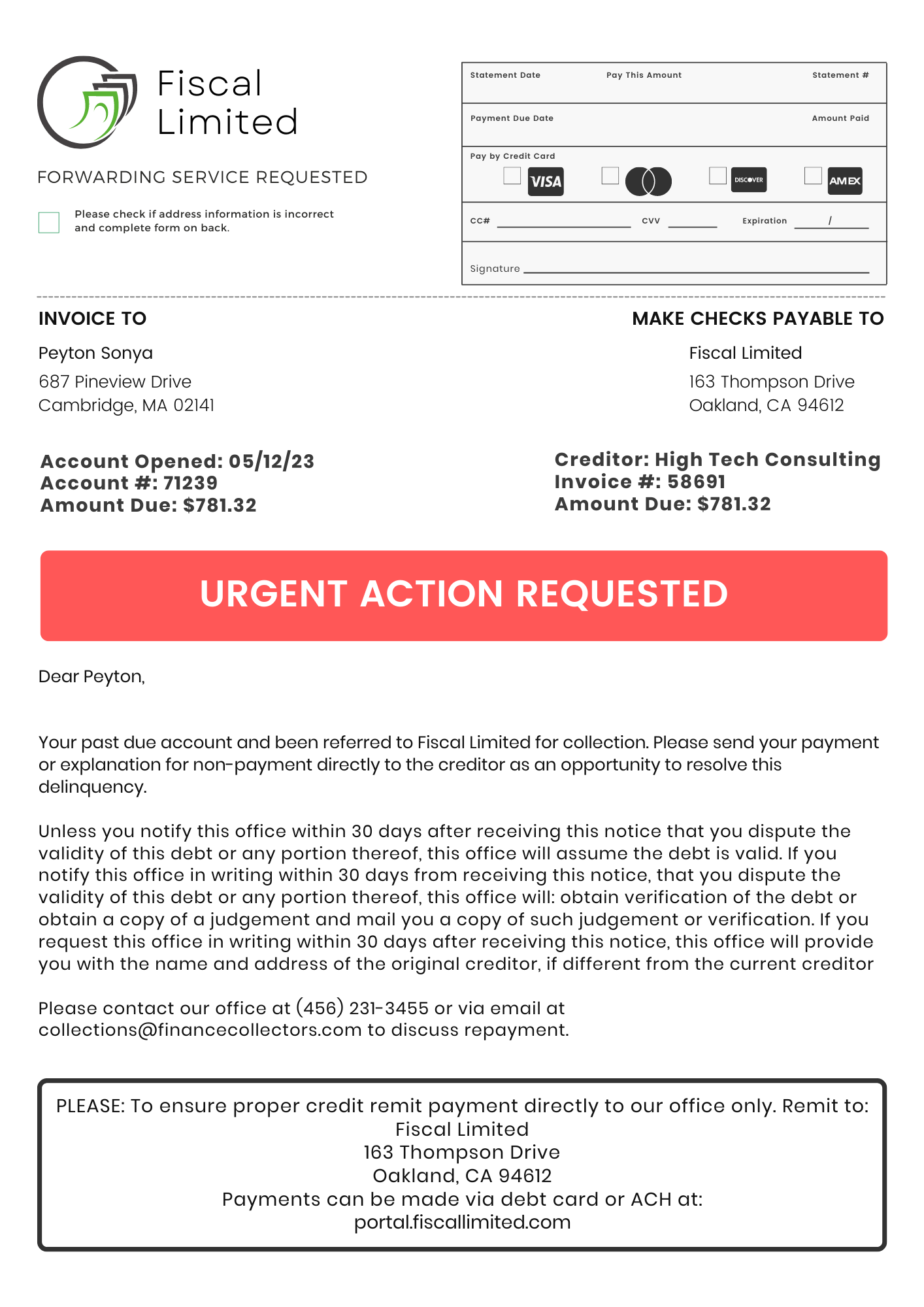

Debt Validation Letter Template 4: Alternative Payment Methods

For the last several decades, the standard payment method for collections has been via cash or check.

If you work for or own a debt collection agency and you still ONLY accept those two methods, you’re making it harder for yourself to complete the promise you give to your clients.

You see, people don’t prefer those two paying methods anymore.

Of transactions made in 2021 (via FRBSF)…

- 28% made via debit card

- 27% made via credit card

- 19% made via cash

In other words, people don’t prefer to pay with cold, hard cash anymore…they prefer paying with plastic.

Thus, if you don’t accept modern forms of payment (including via an online portal) from those who you’re sending your debt validation letters…you’re making it even harder to collect.

The third sample template advertises to the recipient that there are multiple ways to pay off the debt that’s owed.

The way that it’s formatted is key.

Accepting modern payment methods is one thing, but if your recipients can’t figure that out upon first glance…you’re not doing yourself any good. Make it easy to understand for the recipient that there are multiple ways to pay.

Debt Validation Letter Template 5: Alternative Paper Methods

Yes, the standard for sending debt validation letters is a standard 8.5” x 11” piece of paper.

But let’s look at the facts. The average success rate of collections agencies across the country from 1999 to 2010 remained at 17.1%.

What didn’t change between that decade? The industry-standard format for validation letters.

Sure, it’s consistent, but what if there was an alternative that practically guaranteed that your recipients would read it?

That exists, all you have to do is use a postcard.

You see, postcards have a 4.25% open rate. That might not seem like much but it’s almost an entire percentage higher when compared to the 3.5% open rate of letter-sized envelopes.

With those odds, your collection rate will likely cross the 20% range immediately.

The success that postcards see regarding open rates is the reason why the fifth letter example is exactly that…a postcard.

No, it’s not just ANY postcard.

You see, the collections space deals with sensitive personal identification information (PII). If that information were to get into the wrong hands, it could lead to serious consequences for your organization.

But what if I told you that the template postcard in this section prevents leaking PII? It has a secure adhesive peel-off label attached to the front of the letter, which is a safeguard in place to prevent handlers to view the PII inside.

Conclusion

Collection agencies don’t have a choice in sending debt validation letters, they’re a requirement according to the FDCA.

However, that doesn’t mean you need to send two letters to all of your debtors. You can hit the debt validation letter requirements with what you initially sent and it can still help you in your pursuit of satisfying outstanding debts.

You just need a few helpful templates to look at for reference…which you now have by the time you got this far.

Emphasize your product's unique features or benefits to differentiate it from competitors

In nec dictum adipiscing pharetra enim etiam scelerisque dolor purus ipsum egestas cursus vulputate arcu egestas ut eu sed mollis consectetur mattis pharetra curabitur et maecenas in mattis fames consectetur ipsum quis risus mauris aliquam ornare nisl purus at ipsum nulla accumsan consectetur vestibulum suspendisse aliquam condimentum scelerisque lacinia pellentesque vestibulum condimentum turpis ligula pharetra dictum sapien facilisis sapien at sagittis et cursus congue.

- Pharetra curabitur et maecenas in mattis fames consectetur ipsum quis risus.

- Justo urna nisi auctor consequat consectetur dolor lectus blandit.

- Eget egestas volutpat lacinia vestibulum vitae mattis hendrerit.

- Ornare elit odio tellus orci bibendum dictum id sem congue enim amet diam.

Incorporate statistics or specific numbers to highlight the effectiveness or popularity of your offering

Convallis pellentesque ullamcorper sapien sed tristique fermentum proin amet quam tincidunt feugiat vitae neque quisque odio ut pellentesque ac mauris eget lectus. Pretium arcu turpis lacus sapien sit at eu sapien duis magna nunc nibh nam non ut nibh ultrices ultrices elementum egestas enim nisl sed cursus pellentesque sit dignissim enim euismod sit et convallis sed pelis viverra quam at nisl sit pharetra enim nisl nec vestibulum posuere in volutpat sed blandit neque risus.

Use time-sensitive language to encourage immediate action, such as "Limited Time Offer

Feugiat vitae neque quisque odio ut pellentesque ac mauris eget lectus. Pretium arcu turpis lacus sapien sit at eu sapien duis magna nunc nibh nam non ut nibh ultrices ultrices elementum egestas enim nisl sed cursus pellentesque sit dignissim enim euismod sit et convallis sed pelis viverra quam at nisl sit pharetra enim nisl nec vestibulum posuere in volutpat sed blandit neque risus.

- Pharetra curabitur et maecenas in mattis fames consectetur ipsum quis risus.

- Justo urna nisi auctor consequat consectetur dolor lectus blandit.

- Eget egestas volutpat lacinia vestibulum vitae mattis hendrerit.

- Ornare elit odio tellus orci bibendum dictum id sem congue enim amet diam.

Address customer pain points directly by showing how your product solves their problems

Feugiat vitae neque quisque odio ut pellentesque ac mauris eget lectus. Pretium arcu turpis lacus sapien sit at eu sapien duis magna nunc nibh nam non ut nibh ultrices ultrices elementum egestas enim nisl sed cursus pellentesque sit dignissim enim euismod sit et convallis sed pelis viverra quam at nisl sit pharetra enim nisl nec vestibulum posuere in volutpat sed blandit neque risus.

Vel etiam vel amet aenean eget in habitasse nunc duis tellus sem turpis risus aliquam ac volutpat tellus eu faucibus ullamcorper.

Tailor titles to your ideal customer segment using phrases like "Designed for Busy Professionals

Sed pretium id nibh id sit felis vitae volutpat volutpat adipiscing at sodales neque lectus mi phasellus commodo at elit suspendisse ornare faucibus lectus purus viverra in nec aliquet commodo et sed sed nisi tempor mi pellentesque arcu viverra pretium duis enim vulputate dignissim etiam ultrices vitae neque urna proin nibh diam turpis augue lacus.

.avif)