The Massive List of Digital Payment Trends That Are Changing How We All Use Money

In this piece, we identify the biggest trends in digital payment that are changing how we all use money. The way we all grew up buying things is slowing becoming obsolete.

Million of digital payments happen every second across the globe. By 2020, the industry expects to see 726 billion e-payment transactions. Let’s break that number down into more digestible statistics…

- 60.5 billion per month

- Almost 14 billion per week

- Just about 2 billion per day

- Almost 83 million per hour

- Over 23,000 per second

The best part? The number of transactions is growing every year because the industry, as a whole, is so competitive. Consumers have more options to pay right now than they’ve ever had before. So let’s look at the biggest trends driving the growth in digital payments.

Mobile Payments Aren't Stopping

It’s hard to believe that it’s been almost 13 years since the release of the first iPhone. Since then, mobile phone usage has done nothing but climb. Americans not only check their smartphones around 52 times per day but they also prefer their devices for online activities.

The rise of mobile usage naturally increases the rise in mobile payments as well. Business Insider predicts that the volume of mobile payments will increase to $503 billion by 2020.

With those statistics in mind, it’s no wonder there’s been a rise in mobile web-based payments, store app payments, rewards, and SMS-based transactions.

Contactless Payment Rebirth

Have you ever sat in line at the grocery store or a drive-thru and noticed the people in front of your waving their smartphone across a reader? That’s defined as contactless payments and it saves consumers time and it’s been around since the 1990s.

Of course, it’s been slow to catch on in the United States until recently. But in countries like Australia, contactless is king. 98% of all purchases made at fast-food restaurants are contactless down under.

Some of the biggest companies in tech offer their version of contactless payment apps. All a user has to do is download the app they prefer, enter their credit card details, and wave their phone over a reader to make a purchase.

Contactless payment doesn’t stop at mobile phones.

Visa stated that in 2019, banks around the US will issue 100 million contactless Visa cards. Chase is rolling out their tap-to-pay cards this half of 2019.

We can expect this trend to continue to its adoption rate among consumers in the future. Slideing and chipping cards is not nearly as attractive or futuristic as tapping them.

Kiss Your Physical Wallet Goodbye

The apps offered by tech giants mentioned in the section above are called mobile wallets. Essentially their goal is to replace a physical credit card.

Some of the most popular mobile wallets are…

- ApplePay

- Google Pay

- Samsung Pay

- PayPal

It’s predicted a little more than 2 billion consumers will use a mobile wallet to make a purchase in 2019. At that current adoption rate, mobile wallets will overtake cash and credit cards by 2022 across the globe.

Hello P2P Payments

In the past, when your friend forgets their wallet for lunch they’d have to…

- Find their wallet

- Drive to the nearest ATM

- Withdraw cash

- Give it to you

Enter Peer-To-Peer (P2P) payments.

Most mobile wallets offer services allow users to transfer small amounts of money to other users. Due to its convenience, P2P usage continues to skyrocket. By the end of the first quarter of 2019, PayPal’s Venmo processed $21 billion in total payment volume.

But there’s one looming problem that P2P payment organizations face a distrust with older generations.

The majority of P2P users are Millenials and Gen X while Baby Boomers still prefer cash or check payments.

Baby Boomers are more likely to use P2P services from well-known financial institutions. These financial institutions are massive, which is why it’s taken them much longer to join in on the P2P trend.

The Next Generation is Here

As Baby Boomers and Millennials are busy taking wisecracks at each other, a new generation is rising as a majority consumer.

Generation Z is loosely defined as people who were born between 1995 - 2010. This generation doesn’t know a life without the internet or having an instant way of communicating with each other.

Now that they’re in their early to mid-20s they’re expected to account for 40% of all consumers in the United States by 2020, making this group a new powerhouse.

Generation Z prefers person-to-person and business-to-consumer digital payments over other more traditional methods. More specifically, almost 80% of them stated that they use at least one digital payment service every month.

As Uncle Ben from Spider-Man once said, “With great power comes great responsibility.” A statement this generation should keep in mind as they’re heading into their peak years of consumerism.

Purchasing Through Smart Speakers

The smart speaker market is huge and they continue to grow more powerful with new features. They can now do more than just tell you the weather or turn on your lights.

The smart speaker market will grow by $14.4 billion by 2025 and can now make digital purchases with simple voice commands.

One of the main reason why people have smart speakers in the first place is to use them for their purchasing power. It’s predicted that in 2019 31 million people in the United States would make at least one purchase on a smart speaker.

But these devices aren’t stuck in the retail industry. In April 2019, Amazon announced their movement into the healthcare space with Alexa’s Healthcare Skills. One of the skills listed at launch allows users to request notifications when their prescription orders ship.

It’s a safe assumption to make that smart speakers are heading towards allowing users to make digital payments on their healthcare bills.

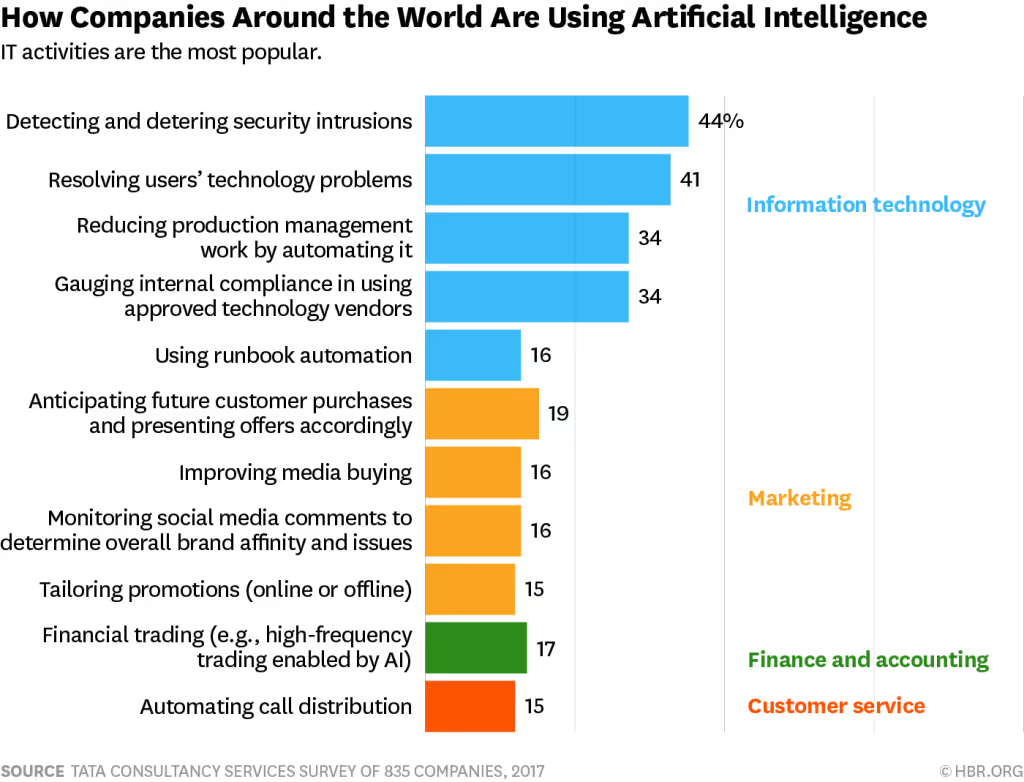

Artificial Intelligence Bloodhounds

There are thousands of digitally processed transactions every second. But what percentage of those transactions are fraudulent?

Every credit card owner at some point will receive a fraud notification from their credit card company. But the systems that identify these purchases don’t always get their predictions right.

Thankfully, those systems are about to get a whole lot smarter.

The most popular use of artificial intelligence is to better detect and deter security intrusions.

Using Biometrics James Bond Style

As the number of devices consumers are using to make payments increases so does the risk of identitfying theft.

Digital payment has gone through three main phases…

- Phase 1 - Users create direct logins to different payment options

- Phase 2 - Users log-in using third-party permissions granted (i.e. Facebook account)

- Phase 3 - Users log-in using biometrics

During the first two phases, users had trouble remembering all their different accounts and passwords. Eventually, this led to people using the same password for their accounts, admit it we have all done this. This practice presented a huge risk, hackers only needed to crack one account to gain access to everything.

The latest security trend in digital payment is using biometrics to verify a user’s identity before making payment.

Most people already accept the concept of using biometrics for payment which makes companies more willing to invest in it. Juniper Research predicts that digital and mobile biometrics will authenticate $2 trillion of sales by 2023.

User Experience is The Golden Ticket

With such a large saturation of ways to make digital payments. A key way companies can differentiate themselves is through their UI/UX.

The last thing clients want when they are trying to pay for something is a tedious process. If it’s more trouble to pay for something than it’s worth, the close button is just a click away.

Consumers don’t like the checkout process, regardless of if it’s through a website or at a physical store. If consumers are more willing to use contactless payment (a section mentioned above) as opposed to swiping their card because it saves them 15 seconds, the user experience that saves them even more time wins.

This trend is also directly related to the buying power Generation Z now possesses. This generation believes their digital experience intertwines with their physical experience. This means that they have greater expectations for not only their payment app’s UX but every app they use.

Gamification and Reward Programs

The two largest consumer cohorts grew up with a now $90 billion video gaming industry. Some digital payment companies realize this opportunity.

Gamifying the payment process makes it both fun and rewarding for digital payment users.

Organizations who are early adopters gamified their process by…

- Providing a small percentage discount the first time a user processes a payment

- Running a “lottery” where every 5th user to process a payment gets cashback on their purchase

Retail giant, Target gamified holiday gift registry building with their Holiday Wish List app. The app used augmented reality to help kids create their wish lists for Santa while at their store. The result was a sales potential of over $92 million.

Global Fintech Expansion

A key digital payment industry buzzword within the banking sector is Fintech, which is a fancy word for financial technology.

Overall, there’s been an explosion of open platforms for developers to use. Some of these platforms are government-backed initiatives. Initiatives such as the European Union’s PSD2 encourages developers to join the industry and create startups.

These new Fintech startups have a particular interest in building solutions for SMBs, a largely underserved group. These SMB’s biggest pain points include…

- Obtaining bank accounts and credit cards

- Expense management

- Payments.

As more Fintech players join the industry, people will continue to have more choices in digital payment.

Blockchain and Cryptocurrency Intrigues

Towards the end of 2017, the hottest news topic for the media and economists from around the world to weigh in on was the rise of Bitcoin. At its peak in December, the cost of one Bitcoin was almost $20,000.

While some early investors of the cryptocurrency cashed in their newfound wealth, digital payment organizations quickly joined the trend. By October 2017, Mastercard announced that it opened-up access to their blockchain API for banks and merchants.

First, Blockchain will continue to trend because of its inherent security. As the main technology behind cryptocurrencies, it removes any need for a central authority. This factor alone makes it impenetrable to hackers.

Next, every transaction that occurs through blockchain contains a fully auditable, valid ledger. This feature alone will cut down financial reporting costs by 70%.

Third, blockchains self-execute smart contracts that no one person controls. The code is what controls the data usage and access which makes everything automatic. It’s so automatic that the technology could reduce infrastructure costs for the majority of the largest investment banks by at least 30%, according to Accenture.

Finally, imagine receiving a paycheck every day after work. Since there is no third-party involvement with blockchain transactions, they can happen in a few seconds.

Chatbot? More Like Cashbot

Have you ever thought of looking up your bank’s Facebook page and depositing money through their chatbot?

You can do that right this very minute on WellsFargo’s Facebook page and it’s been a feature since April 2017.

Instead of having to do the dosi-doe with a customer representative within a chat window, digital payment companies use AI in the form of chatbots.

These chatbots save money for both the organizations who install them and customers who use them. From an organization’s perspective, every call, including those to make a payment or check a balance, costs a company an average of $6. As a bonus, Setting up a chatbot costs less than staffing an entire call center.

From the customers’ standpoint, sometimes there are convenience fees associated with making payments. Chatbots have no usage fees associated with them.

China Sets Sails Toward Global Expansion

China’s popular messaging and digital payments app, WeChat, reached 1 billion daily active users by the end of 2018. Alipay, a Chinese payment and lifestyle app, has over 700 million active users in China.

Both of these apps have their eyes set on the west toward global expansion.

How are they going to grow overseas? Business partnerships.

Alipay has already partnered with companies like JP Morgan Chase and Flutterwave to reach western users.

Partnerships are helpful to Chinese digital payment giants because they can piggyback off of native users. From another standpoint, western companies can take advantage of the growing number of Chinese visitors. In 2017, 4 million Chinese consumers visited North America alone.

Pairing up global partnerships with their already culture-savvy marketing skills packs a powerful digital payment punch.

Payment Request APIs

In 2019, The World Wide Web Consortium (W3C) released its new Payment Request API. This new API allows payment networks to embed themselves into web browsers which makes it easier to introduce new payment types.

The API allows users to make payments with whichever type of currency they want, as long as the merchant accepts the form they’re trying to use. The API also makes digital payment safer. A secure token kept within the browser holds all the payment information.

This token travels across the network to the merchant who maintains the confidential information. It also removes manually entering in payment information which significantly lowers security risks.

These are A Few of My Internet of Things

The term “Internet of Things” (IoT) is a massive buzzword that refers to the ecosystem of computing devices and machines that transfer data over a network. In simpler terms, it refers to the devices that we like to call “smart”.

There’s been an explosion of smart devices that go beyond the aforementioned smart speakers. Here’s a hint, you’re probably wearing one on your wrist.

The future is bright for the smartwatch industry. Statista predicts that the industry’s revenue will grow from $16 billion in 2016 to almost $73 billion by 2022. That’s a 456% increase in revenue within 6 years.

Within the next few years we’ll be living a SciFi lifestyle if that amount of growth continues.

Forbes Tech writer, Vivek Ravisankar, predicts, “With a wave of your hand, your smartwatch detects the translucent cryptography on the milk carton and performs a hash function. The milk is now instantly, irrefutably yours.”

But the IoT doesn’t stop at watches…

- Smart rings can sense your heart rate

- Smart bands can track your workouts

- Smart cars (not the ones created by Mercades) pay at the pump

Each device brings a new way to make digital payment easier while away from the computer.

Defaulting to Paperless Bills

Certain people prefer to send and receive their more important bills through the mail. But in some cases organizations no longer consider their preference.

Massive companies like AT&T converted to paperless bills as their default delivery method in 2019. For their most passionate clients, they can still receive paper bills but have to opt-out of paperless billing first.

As another example, the United States Securities and Exchange Commission (SEC) will allow firms to default to digital delivery of mutual fund reports by 2021.

Making paperless the default will cause headaches for customer service representatives at first. But it may lead to savings on postage and delivery in the long run.

Conclusion

Working in the payment industry, no matter your niche, should cause you jubilation. A lot’s happening that should cause excitement. At their core, all of these trends occur from…

- A new generation of innovators

- Growth in technology

- Progressive changes in government

If each of those continues to happen the payment industry will continue to flourish through this renaissance phase. We can’t wait to see what new trends have yet to come.

Emphasize your product's unique features or benefits to differentiate it from competitors

In nec dictum adipiscing pharetra enim etiam scelerisque dolor purus ipsum egestas cursus vulputate arcu egestas ut eu sed mollis consectetur mattis pharetra curabitur et maecenas in mattis fames consectetur ipsum quis risus mauris aliquam ornare nisl purus at ipsum nulla accumsan consectetur vestibulum suspendisse aliquam condimentum scelerisque lacinia pellentesque vestibulum condimentum turpis ligula pharetra dictum sapien facilisis sapien at sagittis et cursus congue.

- Pharetra curabitur et maecenas in mattis fames consectetur ipsum quis risus.

- Justo urna nisi auctor consequat consectetur dolor lectus blandit.

- Eget egestas volutpat lacinia vestibulum vitae mattis hendrerit.

- Ornare elit odio tellus orci bibendum dictum id sem congue enim amet diam.

Incorporate statistics or specific numbers to highlight the effectiveness or popularity of your offering

Convallis pellentesque ullamcorper sapien sed tristique fermentum proin amet quam tincidunt feugiat vitae neque quisque odio ut pellentesque ac mauris eget lectus. Pretium arcu turpis lacus sapien sit at eu sapien duis magna nunc nibh nam non ut nibh ultrices ultrices elementum egestas enim nisl sed cursus pellentesque sit dignissim enim euismod sit et convallis sed pelis viverra quam at nisl sit pharetra enim nisl nec vestibulum posuere in volutpat sed blandit neque risus.

Use time-sensitive language to encourage immediate action, such as "Limited Time Offer

Feugiat vitae neque quisque odio ut pellentesque ac mauris eget lectus. Pretium arcu turpis lacus sapien sit at eu sapien duis magna nunc nibh nam non ut nibh ultrices ultrices elementum egestas enim nisl sed cursus pellentesque sit dignissim enim euismod sit et convallis sed pelis viverra quam at nisl sit pharetra enim nisl nec vestibulum posuere in volutpat sed blandit neque risus.

- Pharetra curabitur et maecenas in mattis fames consectetur ipsum quis risus.

- Justo urna nisi auctor consequat consectetur dolor lectus blandit.

- Eget egestas volutpat lacinia vestibulum vitae mattis hendrerit.

- Ornare elit odio tellus orci bibendum dictum id sem congue enim amet diam.

Address customer pain points directly by showing how your product solves their problems

Feugiat vitae neque quisque odio ut pellentesque ac mauris eget lectus. Pretium arcu turpis lacus sapien sit at eu sapien duis magna nunc nibh nam non ut nibh ultrices ultrices elementum egestas enim nisl sed cursus pellentesque sit dignissim enim euismod sit et convallis sed pelis viverra quam at nisl sit pharetra enim nisl nec vestibulum posuere in volutpat sed blandit neque risus.

Vel etiam vel amet aenean eget in habitasse nunc duis tellus sem turpis risus aliquam ac volutpat tellus eu faucibus ullamcorper.

Tailor titles to your ideal customer segment using phrases like "Designed for Busy Professionals

Sed pretium id nibh id sit felis vitae volutpat volutpat adipiscing at sodales neque lectus mi phasellus commodo at elit suspendisse ornare faucibus lectus purus viverra in nec aliquet commodo et sed sed nisi tempor mi pellentesque arcu viverra pretium duis enim vulputate dignissim etiam ultrices vitae neque urna proin nibh diam turpis augue lacus.