Long-Term Care Insurance: Coverage, Benefits, and Costs

Long-term care insurance helps cover the costs of extended care services such as home health care, assisted living, and nursing home care. This guide explains how long-term care insurance works, what it covers, how much it costs, and why planning ahead can help protect your savings and ensure you receive care when you need it.

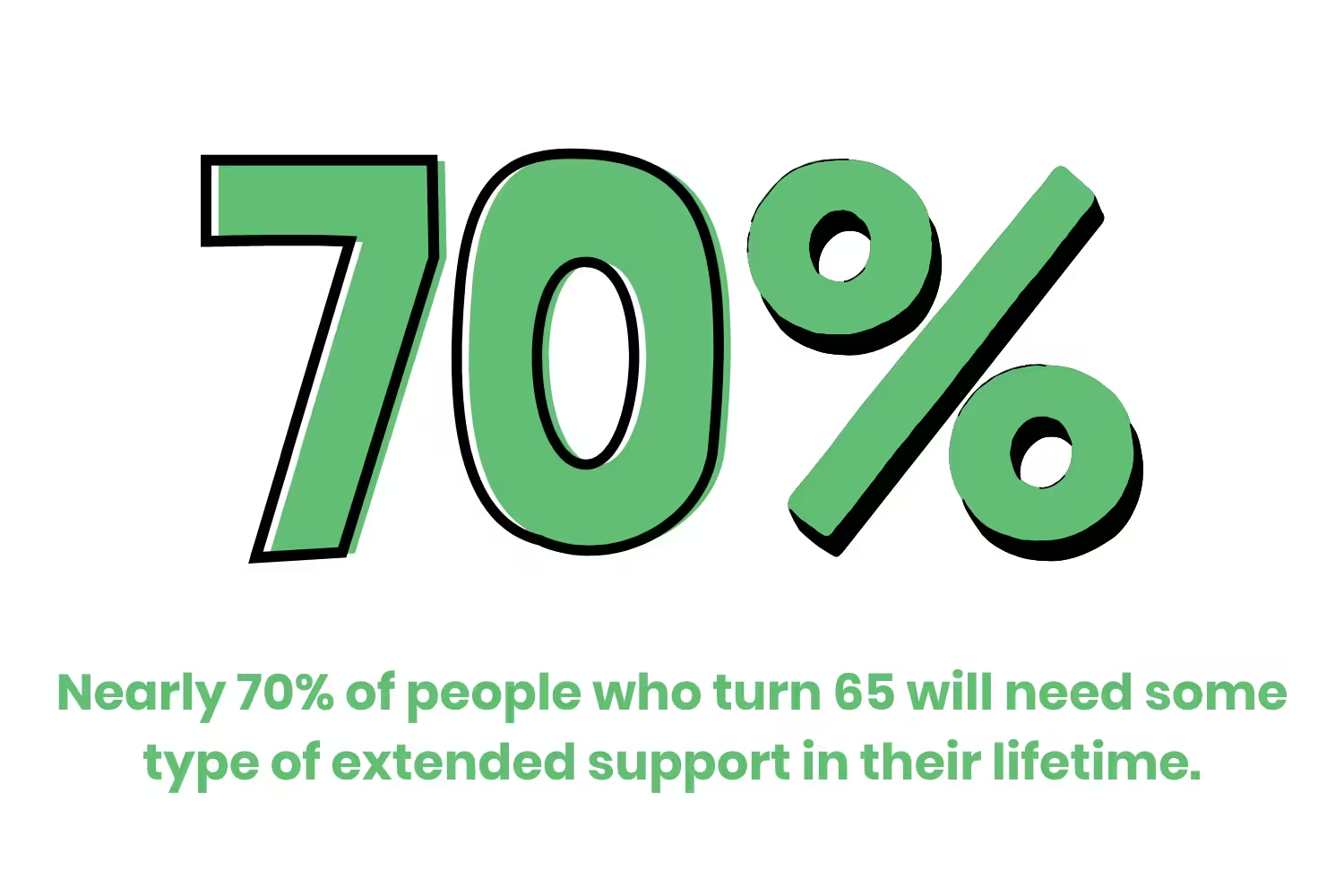

Nearly 70% of people who turn 65 will need some type of extended support in their lifetime, according to the U.S. Department of Health and Human Services. Many believe medicare or private health insurance will pay for this care. In most cases, they do not.

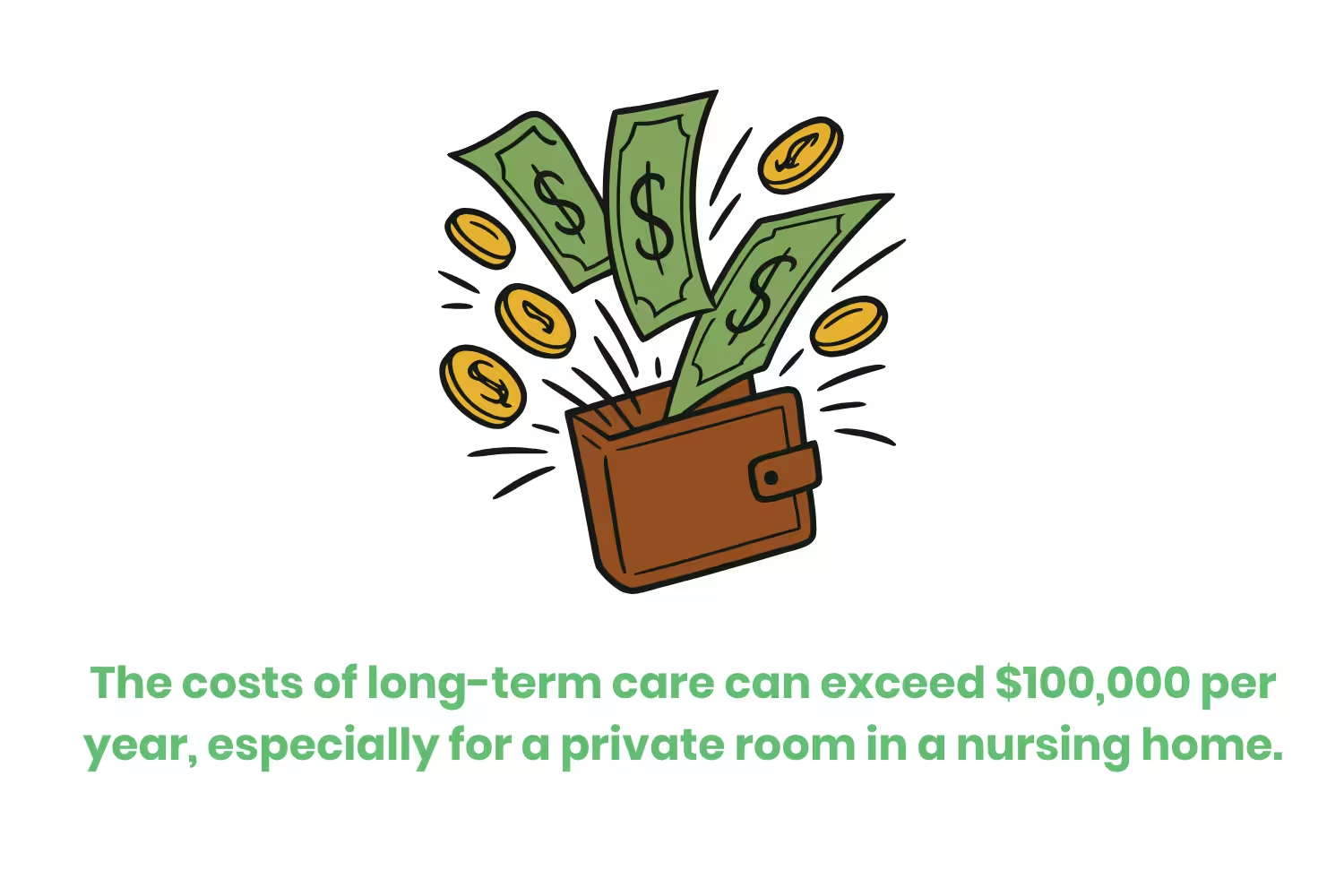

The costs of long-term care can exceed $100,000 per year, especially for a private room in a nursing home. Without a plan, families often pay out of pocket and use up savings. That is why learning about long-term care insurance before you need care is critical.

Planning ahead ensures you can receive care where and how you prefer. It also helps families understand the full costs and benefits of preparing early.

What Is Long-Term Care Insurance and How Does It Work?

Long-term care insurance is designed to help pay for ongoing support when you cannot manage basic daily living tasks. This type of insurance does not replace traditional health insurance or health insurance or medicare. Instead, it focuses on extended assistance, including long-term care provided at home or in a facility.

In simple terms, care insurance offers a way to protect savings while covering future long-term care needs. It helps ensure you can receive care in your home, an assisted living setting, or another supportive environment. It provides structured support for care for people who can no longer live fully independently.

What long-term care services and care services are covered by typical long-term care insurance policies?

Most long-term care insurance policies cover a range of long-term care services. These often include home health care, adult day care, assisted living, and care in a nursing home. Coverage may also apply to assisted living facilities, a skilled nursing facility, and some continuing care retirement communities.

These policies usually cover custodial care, which means help with bathing, dressing, eating, and supervision. This type of care is not typically covered by medicare or traditional health insurance. With strong insurance coverage, you can receive care without placing the full burden on family members.

How do long-term care insurance benefits pay out and what triggers long-term care benefits?

You qualify for long-term care benefits when you cannot perform at least two activities of daily living. These include bathing, dressing, eating, toileting, and transferring. Memory loss can also trigger benefits.

Once approved, insurance benefits are typically paid monthly or daily. The policy will pay up to your selected limit. Some plans reimburse actual care expenses, while others provide fixed payments that allow you to receive care from approved providers.

How do activities of daily living determine eligibility for long-term care coverage?

The six activities of daily living determine when you qualify for long-term care coverage. If you cannot perform two or more without help, you usually qualify.

This rule ensures benefits are available when you truly need long-term care and must receive care on an ongoing basis.

How much does long-term care insurance cost and what affects the premium?

Many people ask how much does long-term care insurance cost. The long-term care insurance cost depends on age, health, and coverage level.

The average annual premium for someone in their 50s is often several thousand dollars. Some individuals pay more if they choose higher daily limits. Your care insurance premiums are based on underwriting and policy features.

When reviewing the cost of a policy, compare it to potential long-term care expenses. These expenses rise quickly once you begin to receive care over an extended period.

Do I need long-term care insurance or will I pay out of pocket?

Many believe they will never need long-term care. However, most older adults will need care at some point. Care may begin with home health care, but some individuals later receive care in assisted living or a nursing home.

Without long-term care insurance, you must pay for long-term care yourself. These rising care costs can reduce retirement savings quickly.

When should you consider purchasing long-term care insurance versus paying for care expenses yourself?

Purchasing long-term care insurance may make sense if you want to protect assets and maintain options for where you receive care. If you have significant wealth, you may choose to pay out of pocket. However, many families face financial strain without insurance coverage.

A financial professional can help you weigh the costs and benefits of each option and review available coverage options.

How likely are you to need care in a nursing home or assisted living facilities and what are the costs of long-term care?

The chance of needing long-term services increases with age. The costs of long-term care depend on location and setting. Assisted living facilities often cost tens of thousands per year. A private room in a nursing home or stay in a skilled nursing facility can cost much more.

Because care may last several years, total long-term care costs can grow quickly as you continue to receive care.

What are the financial risks of not having long-term care insurance and paying out of pocket?

Without insurance coverage, families may use retirement funds or sell assets. Some individuals must spend down savings to qualify for medicaid, which limits choices for where they can receive care.

Planning ahead helps manage unexpected long-term care needs and ensures you can receive care in a setting that fits your preferences.

What types of long-term care insurance and insurance program options are available?

There are several types of long-term care policies available.

Traditional long-term care policies focus only on care services.

Hybrid long-term care insurance combines life insurance with long-term care protection. These hybrid policies may include a long-term care rider attached to a life insurance policy, often structured within permanent life insurance. These policies allow access to long-term care benefits with life coverage, meaning you can use benefits to receive care or leave funds to family if you never need long-term care.

Some employers offer a long term care insurance program or access to federal long term care insurance. These structured plans are a type of organized insurance program. Educational support is available through the American Association for long-term care and the association for long-term care insurance.

How do life insurance policy riders and permanent life insurance compare to standalone long-term care insurance policies?

Standalone long-term care insurance policies focus only on care. Policies that include insurance with long-term care benefits allow you to combine long-term care benefits with a death benefit.

Your decision should reflect your budget, goals, and expected long-term care needs, as well as where you prefer to receive care in the future.

How to purchase and qualify for long-term care insurance: purchasing long-term care insurance

To qualify for long-term care insurance, you must complete medical underwriting. Insurers review health history and medications. Some people may not qualify for long-term coverage.

When purchasing long-term care insurance, review elimination periods and benefit limits. Check your state insurance department to confirm licensing. Careful review ensures you can receive care without unexpected coverage gaps.

How will long-term care insurance interact with Medicare and other programs?

Medicare does not usually cover long-term care. It may pay for short stays in a skilled nursing facility, but not ongoing custodial care.

How do long-term care insurance benefits coordinate with Medicaid or other government programs when you need care?

If savings run out, some individuals qualify for medicaid, which covers certain long-term services. However, strict income and asset rules apply.

Having long-term care insurance can delay reliance on Medicaid and expand your options for where you receive care.

What planning strategies help cover long-term care costs and ensure long-term care coverage when needed?

Strong planning for long-term care may include buying long-term care insurance, selecting hybrid long-term care insurance, or saving funds to cover long-term care.

Early planning prepares you for future long-term care needs while protecting financial stability and ensuring you can confidently receive care when needed.

Conclusion

Long-term care insurance can provide protection against rising long-term care costs. Because long-term care insurance offers structured insurance benefits, and it helps families pay for care without draining savings.

The key question is not whether you might someday need long-term care. It is whether you are financially prepared to receive care in the setting you choose when those long-term care needs arise.

Emphasize your product's unique features or benefits to differentiate it from competitors

In nec dictum adipiscing pharetra enim etiam scelerisque dolor purus ipsum egestas cursus vulputate arcu egestas ut eu sed mollis consectetur mattis pharetra curabitur et maecenas in mattis fames consectetur ipsum quis risus mauris aliquam ornare nisl purus at ipsum nulla accumsan consectetur vestibulum suspendisse aliquam condimentum scelerisque lacinia pellentesque vestibulum condimentum turpis ligula pharetra dictum sapien facilisis sapien at sagittis et cursus congue.

- Pharetra curabitur et maecenas in mattis fames consectetur ipsum quis risus.

- Justo urna nisi auctor consequat consectetur dolor lectus blandit.

- Eget egestas volutpat lacinia vestibulum vitae mattis hendrerit.

- Ornare elit odio tellus orci bibendum dictum id sem congue enim amet diam.

Incorporate statistics or specific numbers to highlight the effectiveness or popularity of your offering

Convallis pellentesque ullamcorper sapien sed tristique fermentum proin amet quam tincidunt feugiat vitae neque quisque odio ut pellentesque ac mauris eget lectus. Pretium arcu turpis lacus sapien sit at eu sapien duis magna nunc nibh nam non ut nibh ultrices ultrices elementum egestas enim nisl sed cursus pellentesque sit dignissim enim euismod sit et convallis sed pelis viverra quam at nisl sit pharetra enim nisl nec vestibulum posuere in volutpat sed blandit neque risus.

Use time-sensitive language to encourage immediate action, such as "Limited Time Offer

Feugiat vitae neque quisque odio ut pellentesque ac mauris eget lectus. Pretium arcu turpis lacus sapien sit at eu sapien duis magna nunc nibh nam non ut nibh ultrices ultrices elementum egestas enim nisl sed cursus pellentesque sit dignissim enim euismod sit et convallis sed pelis viverra quam at nisl sit pharetra enim nisl nec vestibulum posuere in volutpat sed blandit neque risus.

- Pharetra curabitur et maecenas in mattis fames consectetur ipsum quis risus.

- Justo urna nisi auctor consequat consectetur dolor lectus blandit.

- Eget egestas volutpat lacinia vestibulum vitae mattis hendrerit.

- Ornare elit odio tellus orci bibendum dictum id sem congue enim amet diam.

Address customer pain points directly by showing how your product solves their problems

Feugiat vitae neque quisque odio ut pellentesque ac mauris eget lectus. Pretium arcu turpis lacus sapien sit at eu sapien duis magna nunc nibh nam non ut nibh ultrices ultrices elementum egestas enim nisl sed cursus pellentesque sit dignissim enim euismod sit et convallis sed pelis viverra quam at nisl sit pharetra enim nisl nec vestibulum posuere in volutpat sed blandit neque risus.

Vel etiam vel amet aenean eget in habitasse nunc duis tellus sem turpis risus aliquam ac volutpat tellus eu faucibus ullamcorper.

Tailor titles to your ideal customer segment using phrases like "Designed for Busy Professionals

Sed pretium id nibh id sit felis vitae volutpat volutpat adipiscing at sodales neque lectus mi phasellus commodo at elit suspendisse ornare faucibus lectus purus viverra in nec aliquet commodo et sed sed nisi tempor mi pellentesque arcu viverra pretium duis enim vulputate dignissim etiam ultrices vitae neque urna proin nibh diam turpis augue lacus.

![[ANSWERED] What Does a Clearinghouse Do During Claim Submissions?](https://cdn.prod.website-files.com/67e2b8210878abcba6f91ae6/68aced47fd2f60af75b002b6_WhatDoesaClearinghouseDoDuringClaimSubmissions_1023.avif)